Juncture Wealth Strategies - Year Ahead Commentary for 2026

2026 Economic & Market Forecast

- Economy

- Inflation

- Bond Markets

- Equity Markets

- 2026 Predictions

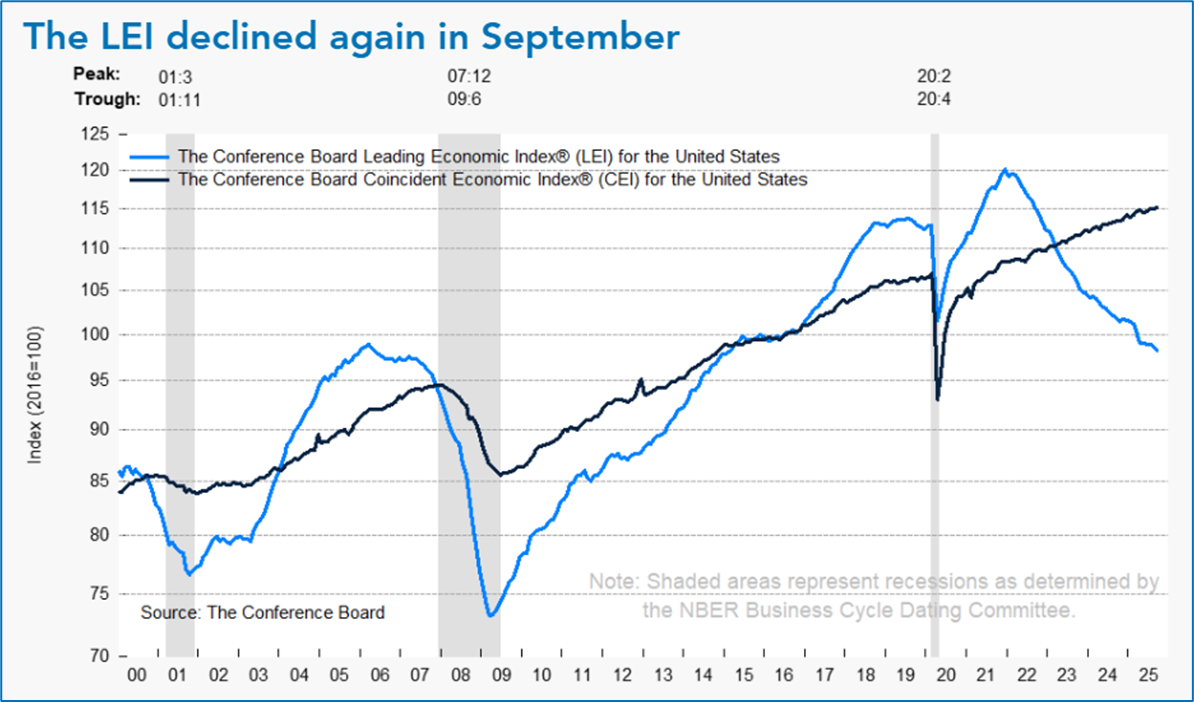

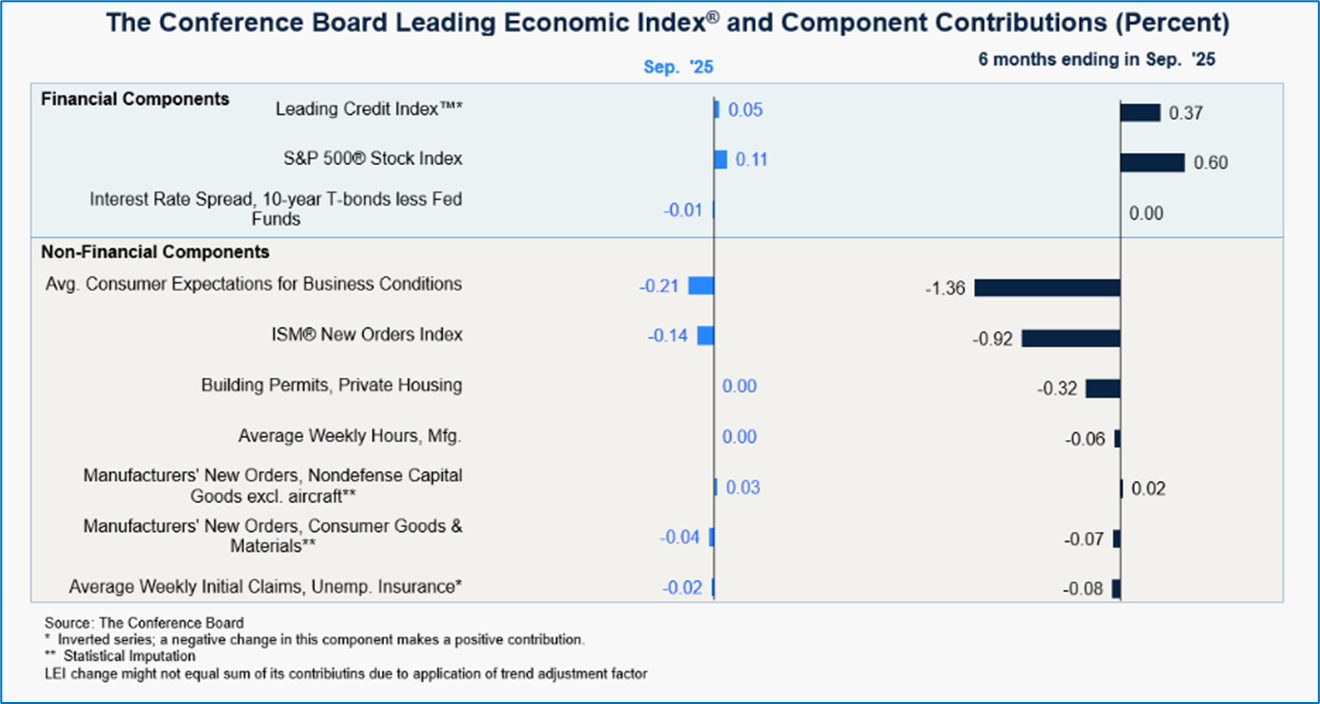

Economy: Leading Economic Indicator (LEI)

The Leading Economic Indicator continues to signal weakness in the US economy in 2026. The chart shows the divergence between the current versus future expected economic growth. The Coincident Economic Index indicates that current economic activity is at a much higher level than survey participants expect in the next six to twelve months.

Economy: Leading Economic Indicator (LEI)

The Leading Economic Indicator continues to signal weakness in the US economy. The below chart shows that the US has struggled with recession-like conditions in some sectors. The slowdown has been broad-based with only the stock and bond market positively contributing to growth. The LEI may not capture the full effect of labor-enhancing technology which increases corporate earnings. Higher corporate earnings contribute to higher stock prices. Higher stock prices increases household wealth which encourages spending. This may impact 2026 economic growth relative to current expectations.

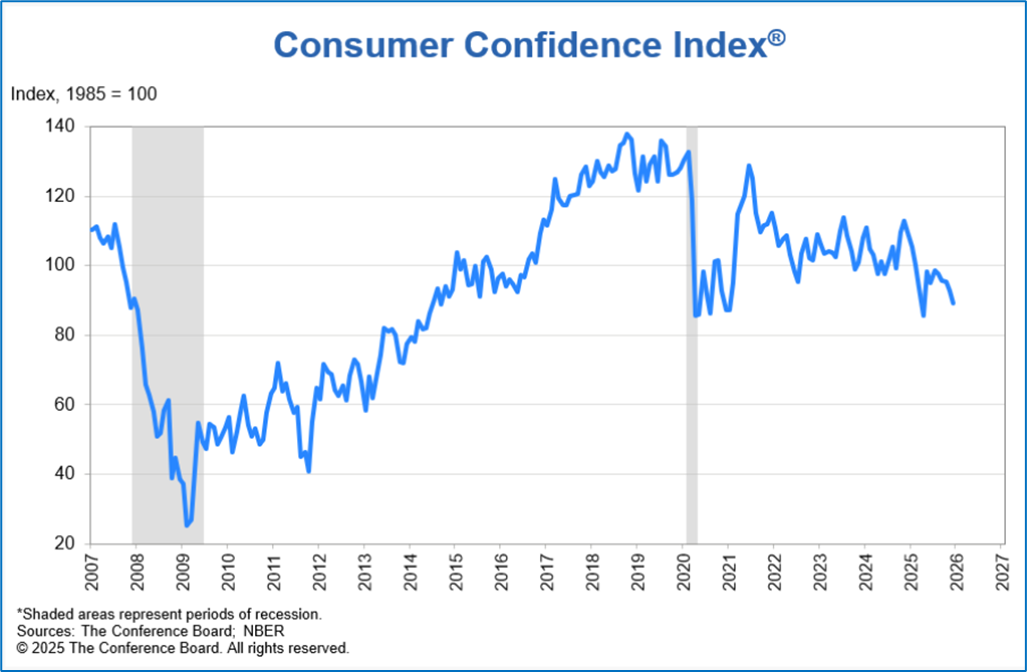

| Economy: Consumer Confidence Consumer confidence has been depressed even in the face of higher wages, a surging stock market and a growing economy. It is possible that households beginning to cope with lower savings. Generally, investors tend to swing from overly optimistic to overly pessimistic depending on the most recent environment. In this case, fewer jobs. Fewer available jobs cause consumers to worry about paying for the lifestyles whether it be food, housing, gas or entertainment. This worry can lead to fear of investing as consumers may need available cash to pay for expenses rather than invest for long-term goals. Fear may also keep most stocks from being fairly-priced as the marginal investor isn’t buying. These conditions may describe our current situation even though the job market has normalized and interest rates are expected to be reduced this year. |  |

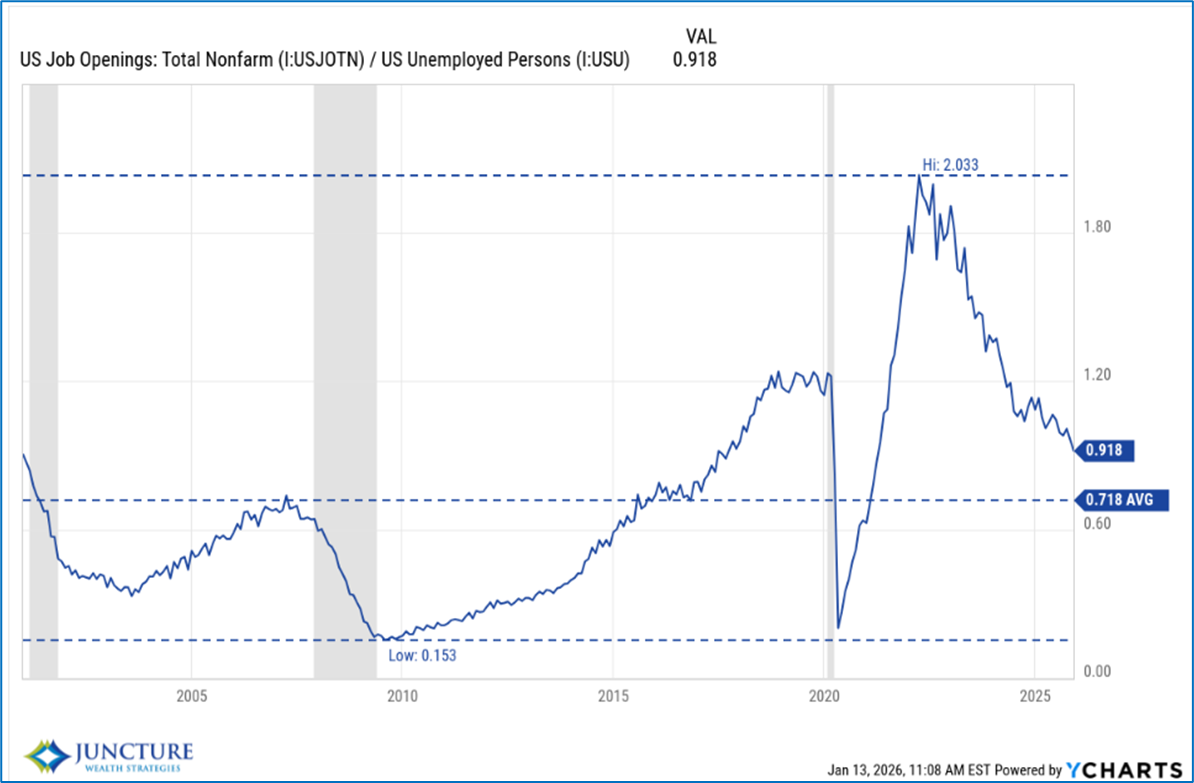

| Economy: Jobs Consumer confidence has been shaky this year as consumers focused on a weaker job market even while the US has 0.9 job openings per unemployed worker in the US. This 0.9 job openings to unemployed worker exceeds the 20-year average of 0.72 jobs per unemployed worker. However, it is much lower than its peak of 2.0 set in March 2022 when companies found it difficult to recruit and retain employees due to the pandemic era relief financial support. One fear is that Artificial Intelligence will replace workers. Eventually, it will. It will also create other jobs. We do not see job market weakness negatively impacting the economy this year. |  |

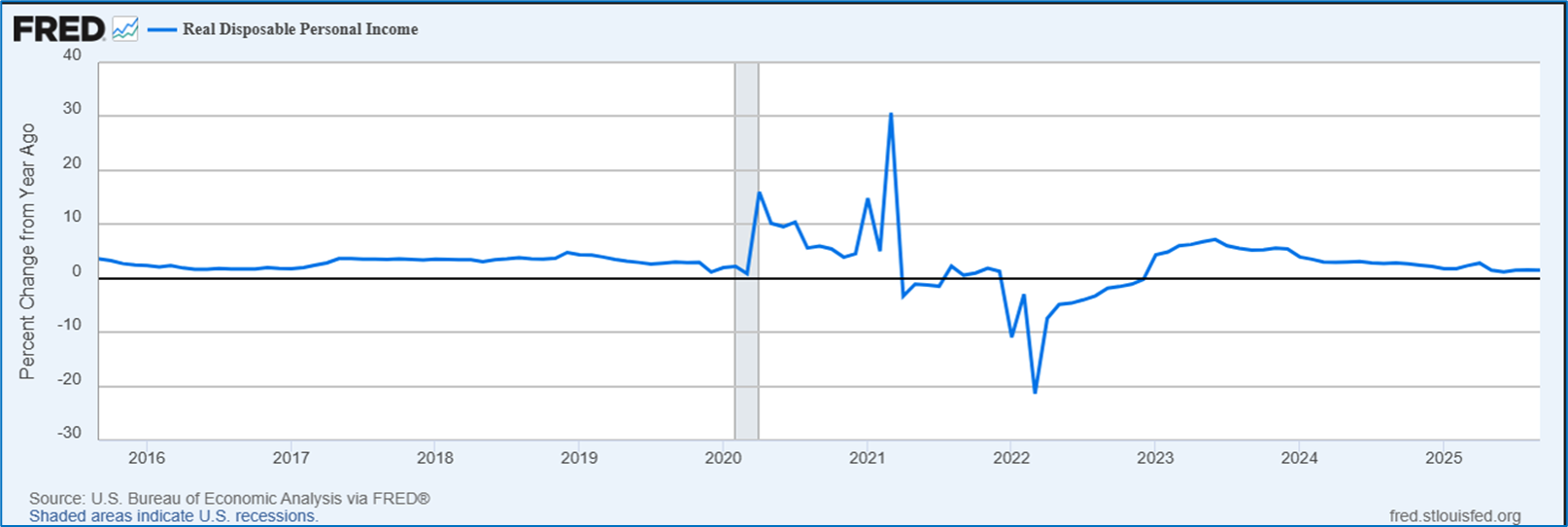

Economy: Consumer Confidence

Another factor that households may be discounting in the Consumer Confidence survey is that real disposable income has been growing since 2023. This means that households' income growth is exceeding inflation by approximately 1.5% which should be supportive of household spending.

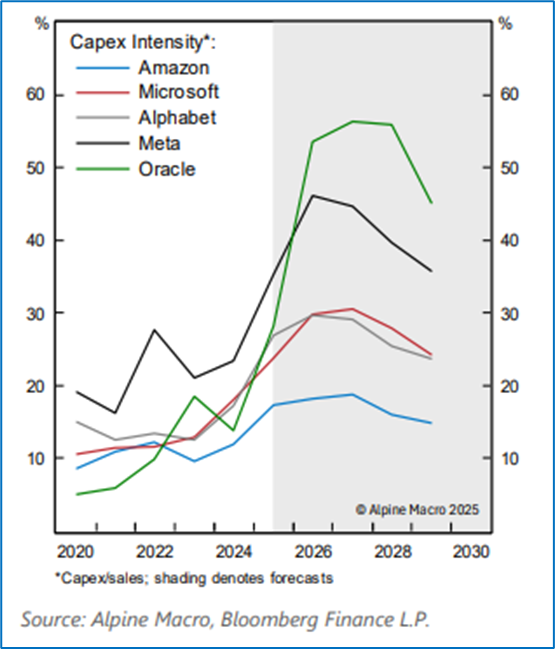

Economy: Artificial Intelligence

The last three years have introduced many investors to artificial intelligence (AI) models. To continue this progress, technology companies have announced massive capital expenditure programs aimed at building AI infrastructure: chips, servers, data centers, energy producers. It is estimated that companies will invest roughly $500 billion in 2026 most of which is funded from current operating cash flows. The media may begin to focus on other themes as the infrastructure takes time to build. Once the infrastructure is built, we will enter the second phase of the innovation wave: applications. During this phase, AI, robotics and mobility solutions will converge to transform our work and home lives in unexpected ways.

|  |

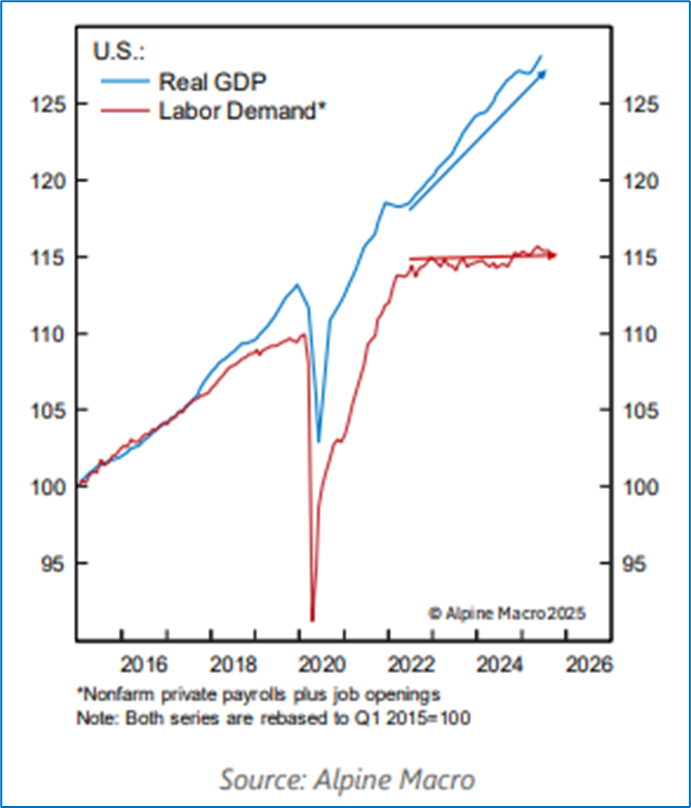

| Economy: Artificial Intelligence The level of AI investment will help support US and global productivity and economic growth in 2026. Increased productivity may help companies maintain and grow their profit margins by restraining overall labor costs. The chart to the right shows how companies have been relying on technology to keep headcount (red line) manageable even as the economy (blue line) has expanded significantly since 2022. Companies will continue to become more efficient as AI replaces humans; initially taking over repetitive tasks but progressing to more difficult ones. This trend could accelerate as AI begins to converge with robotics and mobility solutions in future years. |  |

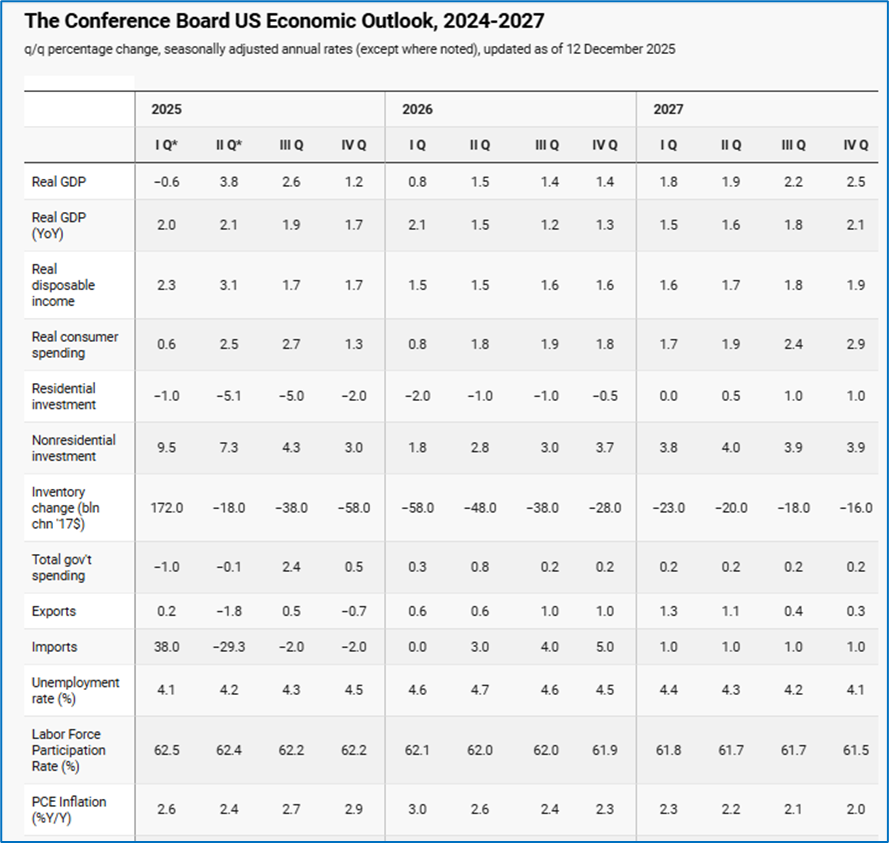

Economy: US Gross Domestic Product (GDP) The Conference Board’s 2026 US Economic Outlook suggests that the US real GDP growth will hit its low in the first quarter of 2026. After that point, it should strengthen over the next three quarters to average 1.5%. Our economy in 2026 partially relies on the capital expenditures, solid real disposable income, and solid household balance sheets. We continue to believe these trends will continue to support the US economy over the next few years. In conclusion, the economy will hit its nadir in the first part of the year and strengthen in the last half. The risk may be to an upside surprise if the consumer and productivity remains strong while capital expenditures continue their high pace. |  |

Inflation: Money Supply

Money supply is the fuel for inflation over a long period of time. We analyze the change in various money supply measures to assess the likelihood of future, persistent inflation. The M2 which is comprised of M1 (currency, checking and savings accounts) plus money markets and small CDs has settled into a typical 4.5% annual growth rate.

Inflation: Expected Inflation 2026

The expected inflation for 2026 currently is 3.19%. It has increased from 2.2% in March 2025 to 3.19% in December 2025. A combination of increased tariff impact, decreased labor supply, and greater fiscal impulse have caused households and investors to expected stronger inflation in the year ahead. Shelter inflation should moderate the increase due to declining new rents in most markets. We could see an inflation surprise to the downside if labor market conditions worsen.

Bond Markets

Bond yields are an important factor for the economy as they represent cost of financing for companies and governments which need to raise capital. Investors begin to price in stable rates as the Federal Reserve may pause any rate decreases until the Fed sees evidence of a slowing economy or continuing disinflation. A key risk is that inflation comes in higher than expected and the bond market’s predictions of two interest rate decreases turn out to be too optimistic. The chart below shows that investors lack confidence in bond yield outcomes and, as such, are sticking with a range-bound yield forecast.

Bonds: Future Interest Rates

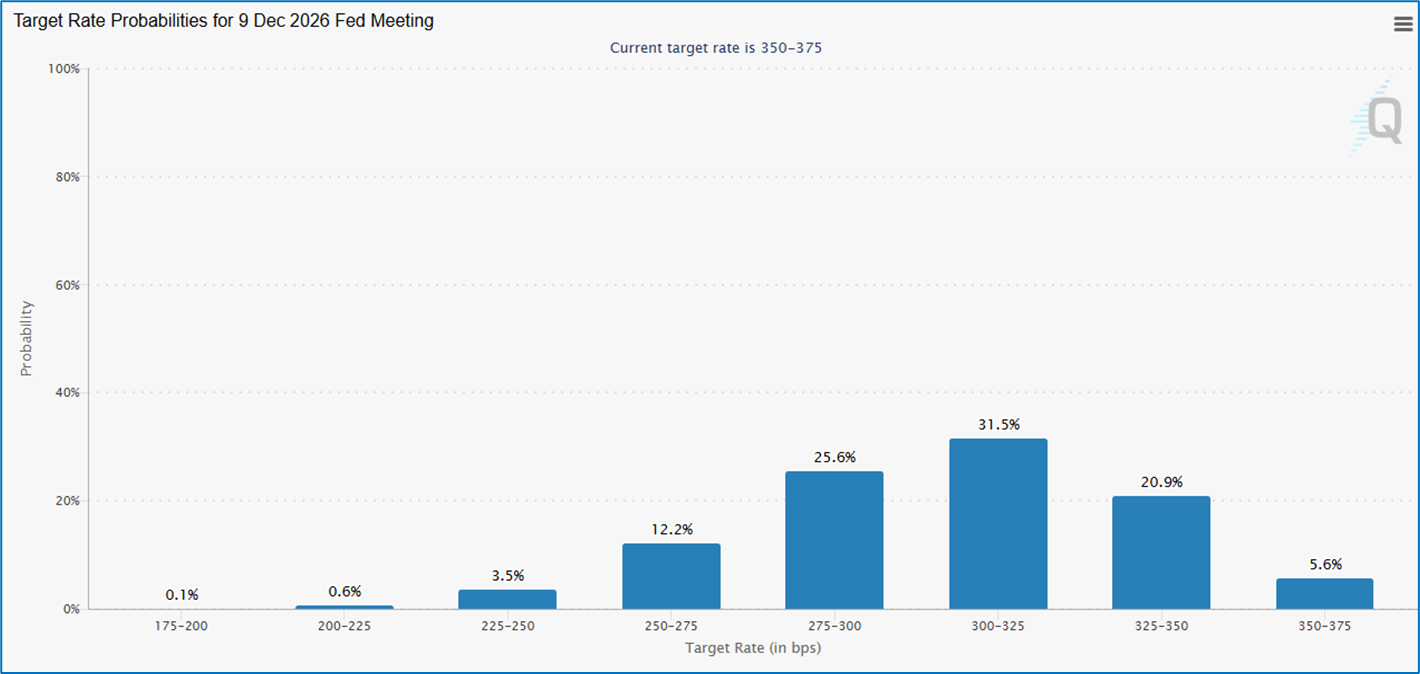

Bond traders have begun to price in lower interest rates in response to weaker job market conditions. This chart shows that futures markets are currently projecting one to two interest rate decreases this year. This is a volatile measure and will change as more economic data is reported. We expect the Federal Reserve to hold interest rates steady until data confirms direction in economic conditions.

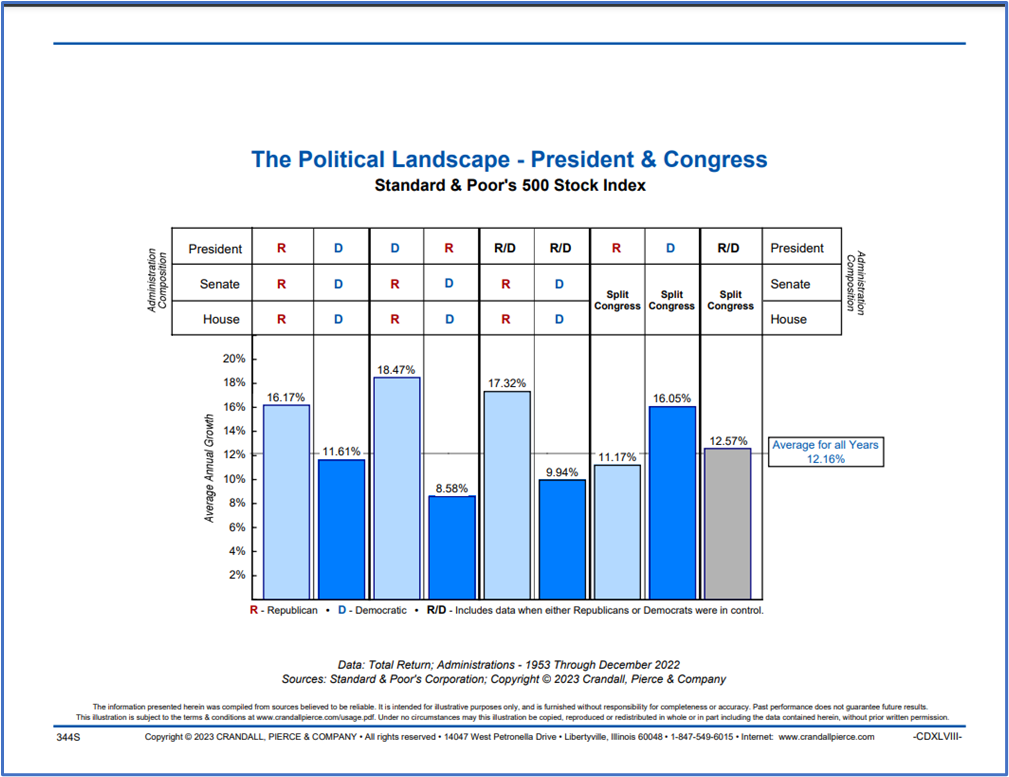

| Equities: Election Year Returns In the current divisive political environment, each political party may frame the opponent’s victory as disaster for the economy and stock market. It is important to put these comments in perspective. Historically, the stock market has experienced decent returns with a Republican president and split Congress (see chart). The worst relative returns were seen in years when a Republican President was combined with a Democratic Congress. None of the compositions were a disaster for the US economy nor the US equity market. Elections can cause fear among voters which may cause them to change their investment allocations. This volatility should be short-term in nature. In conclusion, we expect equities, overall, to have a good year as more stocks begin to participate. At the same time, we expect the Mag 8 (& cap weighted indices) to lag this rally while we experience a transition from mega cap to large/small/mid cap stocks. |  |

Geopolitics

We expect geopolitics to create larger risks to asset markets. The various conflicts and wars have the potential to expand in size and scope as they may pull in other global participants. We are monitoring the situations very closely since they may significantly impact global economies and asset markets. We continue to expect geopolitics to be a significant source of risk this year.

|  |  |

|  |  |

JWS Prediction | |

Equities | •Leadership transition from mega cap stocks to large, small- and mid-cap stocks. •Mag 8 to lag while market participation broadens. •Global stocks may begin to rally if the global economy begins to accelerate. •Emerging markets may continue to perform well. |

Fixed Income | •High credit, long duration, fixed rate to outperform. •Stable to lower yields should be expected across the maturity curve as short-term yields drop relative to long-term yields. |

Real Assets | •Commodities may begin to offer better returns once global economy begins to accelerate. •Industrial metals may lead as AI infrastructure build progresses. |

GDP Growth | •GDP growth should accelerate in second half of year as the interest rate decreases from last year begin to encourage activity. |

Inflation | •Inflation continues to be higher than 2% target. |

Interest Rates | •The Fed may pause interest decreases until economic data provides direction of labor market and inflation. |

Geopolitics | •Russia/Ukraine •China •Venezuela •Global relations always has a potential for conflicts which have not yet begun. |