Juncture Wealth Strategies - February 2021 Market Update

COVID-19 Pandemic

From the latest Situation Report by the World Health Organization, the number of new cases and deaths has continued to fall significantly. Is the decline due to vaccinations, herd immunity or social distancing measures? The answer will significantly affect the global economy. Only time will tell us the answer.

|  |

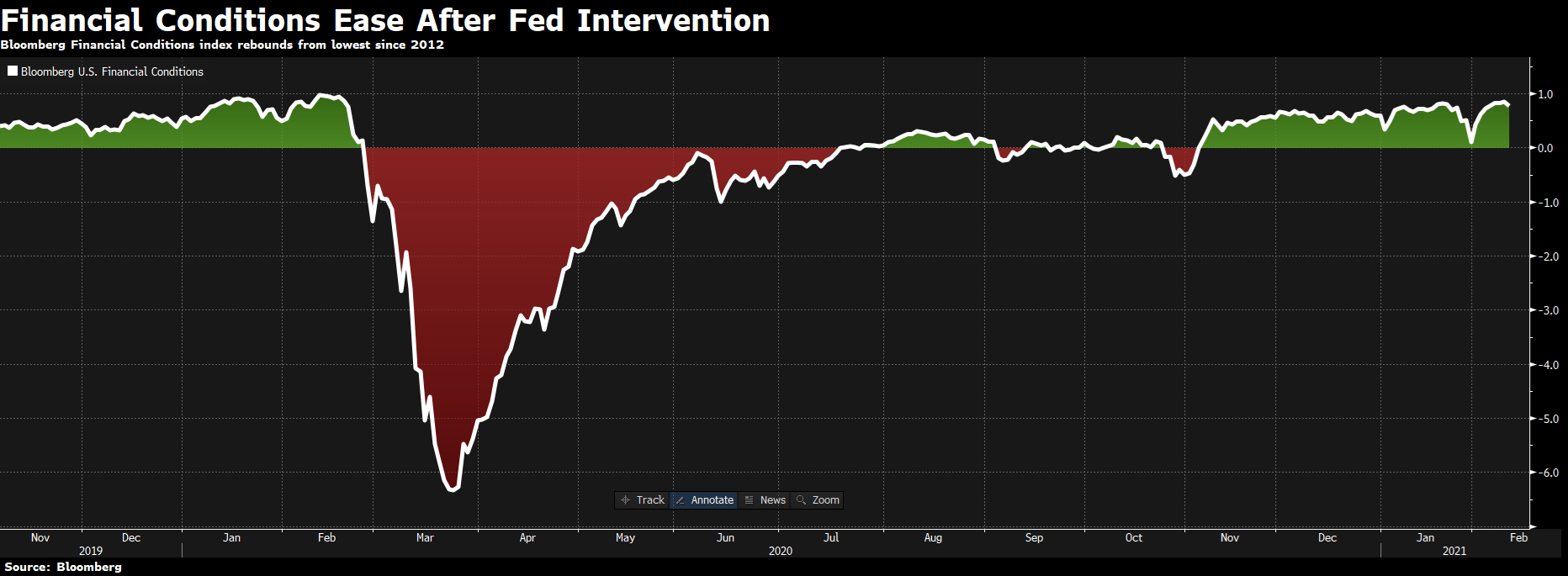

Are Investors Complacent?

Financial Conditions continue to be “easy”. We expect that the liquidity will remain plentiful as the Federal Reserve & Congress continue to underpin the economy and the workers harmed by the pandemic.

Expected Inflation

With the ample liquidity in the economy, many investors and consumers have been discussing the possibility of higher inflation. As shown below, expected inflation beginning in three years have increased to approximately 3%. This is a positive for most investors and consumers. We need to monitor the situation as the economy reopens.

US Expected Real Interest Rate

The real interest rate in the US is the nominal rate adjusted for expected inflation. Since 1997, the highest real interest rate was 4.1% and the low was -1.98%. We are currently -1.89%. This essentially tells investors that the cost of debt is negative since inflation offsets the interest rates. This low cost of funding should continue to support business and consumer spending.

Fed Reactions?

One of the risks to the equity market is the potential for the Federal Reserve to begin to taper its asset purchases and/or raise interest rates. They have indicated the FOMC will remain on hold until inflation becomes problematic. We still have yet to see inflation, but if we see higher persistent inflation, we could see the Fed act earlier than many investors expect. This earlier action would put the equity and bond market rallies at risk.

|  |

Temper Tantrum?

Given the backdrop of plentiful liquidity causing negative real yields on bonds and the potential for future inflation, we need to vigilant to the Federal Reserve’s intention for future action. As shown below, the Federal Reserve can cause significant volatility in the fixed income markets when they announced their intent to begin to taper. In Dec 2013, they initiated the taper. As you can see, the 10-year US Treasury yield doubled from its low rate in 2012. The potential for bond yields to react negatively to Fed actions is important for investors to keep in mind. It would also become a headwind for most equities.

US Dollar

The USD has dropped since the beginning of 2020 as record amounts of stimulus were pumped into the economy. With the continued monetary support and potential federal stimulus, we expect the USD to remain under pressure and, possibly, to continue to move lower. A weakening USD may provide support for International/Emerging Market assets and Commodities to outperform.

How should we be positioned?

Small Cap is continuing to lead since Oct 2020. This is an important development since small businesses are the ones most impacted by lockdowns. We are maintaining our small cap overweight until we see changes in liquidity in the markets.

Earnings Growth

Small cap companies are outperforming their large cap counterparts significantly year to date. One of the reasons is because earnings for small companies suffered more than large companies last year. This year, small companies are expected to return to earnings growth as analysts revise their earnings estimates higher.

How should we be positioned?

Below are a few of the charts we follow to see the shifts in certain equity markets. In the top chart, Emerging Market stocks are outperforming US large cap companies. Developed Markets (MSCI EAFE) are slowly beginning to gain some outperformance after years of underperformance.

How should we be positioned?

Value has moderated somewhat versus Growth but has a long way to go before increasing our exposure is considered prudent.

Summary

- The Fed has stabilized the financial markets via substantial liquidity interventions.

- Interest rates should remain low for longer underpinning support for equity and short-term bond markets.

- Negative real yields will encourage international investors to invest in assets denominated in other currencies causing the US Dollar to struggle.

- Fiscal stabilization packages will be needed in the short term until vaccines and/or herd immunity can be reached.

- Earnings are expected to growth significantly over the next two years with Small Cap & Emerging Markets continuing their leadership role.

- Begin to look for inflation to slowly build in second half of 2021 into 2022.

Action Plans

- Overweight Small Cap companies relative to Large Cap.

- Begin to gain exposure to cyclically-sensitive sectors and companies.

- Begin to build positions in International and Emerging Market equities and fixed income.

- Increase exposure to Commodities.

- Employ a hedging strategy to moderate downside risk, if necessary.

Disclaimer: This newsletter is provided to you for informational purposes only. Any specific firm or security presented should not be construed as an endorsement or recommendation by Juncture Wealth Strategies, LLC. No advice may be rendered by Juncture Wealth Strategies, LLC unless a client service agreement is in place. Please consult with your financial advisor before making any investment. Information provided by Bloomberg is believed to be accurate but has not been verified